Exhibit 99.1

|

|

INVESTIndiana Conference September 2014 Pursuing Growth • Building Value a global diversified industrial company |

Exhibit 99.1

|

|

INVESTIndiana Conference September 2014 Pursuing Growth • Building Value a global diversified industrial company |

|

|

Forward-Looking Statements and Factors That May Affect Future Results: Throughout this presentation, we make a number of “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. As the words imply, these are statements about future plans, objectives, beliefs, and expectations that might or might not happen in the future, as contrasted with historical information. Forward-looking statements are based on assumptions that we believe are reasonable, but by their very nature are subject to a wide range of risks. Accordingly, in this presentation, we may say something like, “We expect that future revenue associated with the Process Equipment Group will be influenced by order backlog.” That is a forward-looking statement, as indicated by the word “expect” and by the clear meaning of the sentence. Other words that could indicate we are making forward-looking statements include: This is not an exhaustive list, but is intended to give you an idea of how we try to identify forward-looking statements. The absence of any of these words, however, does not mean that the statement is not forward-looking. Here is the key point: Forward-looking statements are not guarantees of future performance, and our actual results could differ materially from those set forth in any forward-looking statements. Any number of factors, many of which are beyond our control, could cause our performance to differ significantly from what is described in the forward-looking statements. For a discussion of factors that could cause actual results to differ from those contained in forward-looking statements, see the discussions under the heading “Risk Factors” in Item 1A of Part II our Form 10-Q for the period ended June 30, 2014, located on our website and filed with the SEC. We assume no obligation to update or revise any forward-looking statements. Disclosure regarding forward-looking statements 2 |

|

|

Agenda Hillenbrand a global diversified industrial company Process Equipment Group (PEG) our growth business platform Batesville our time-tested and highly profitable market leader Select Financial Results 3 |

|

|

Hillenbrand is an attractive investment opportunity Market leading platforms with robust cash generation Strong balance sheet and cash flow Process Equipment Group represents ~2/3 of Hillenbrand revenue with attractive organic mid to high single-digit growth expected Bottom-line growth enhanced by leveraging core competencies Meaningful return of cash to shareholders, including an attractive dividend yield Annual dividend increases since HI inception (2008) Strong Financial Profile Growth Opportunity Compelling Dividend Proven Track Record Demonstrated acquisition success Proven, results-oriented management teams Strong core competencies in lean business, strategy management and talent development 4 |

|

|

Hillenbrand Profile 5 |

|

|

Hillenbrand began as a death care company and has diversified through acquisitions Leading global providers of compounding and extrusion equipment, bulk solids material handling equipment and systems for a wide variety of manufacturing and other industrial processes Serves customers through its operating companies: Coperion – Compounders and extruders, materials handling equipment, feeders and pneumatic conveying equipment, system solutions, parts and services (K-Tron merged with Coperion effective 10/1/2013) Rotex – Dry material separation machines and replacement parts and accessories TerraSource Global– Size reduction equipment, conveying systems and screening equipment, parts and services Founded in 1906 and dedicated for more than 100 years to helping families honor the lives of those they love® North American leader in death care with a history of manufacturing excellence, product innovation, superior customer service, and reliable delivery 2007 2008 2009 2010 Hillenbrand Industries approves the separation of Hill-Rom and Batesville Casket into two independent publicly traded companies Hillenbrand, Inc. (parent of Batesville Casket Company) begins operation April 1, 2008 K-Tron Acquisition (includes TerraSource) April 1, 2010 Batesville Process Equipment Group 2011 Rotex acquisition September 1, 2011 2012 Coperion acquisition December 1, 2012 6 |

|

|

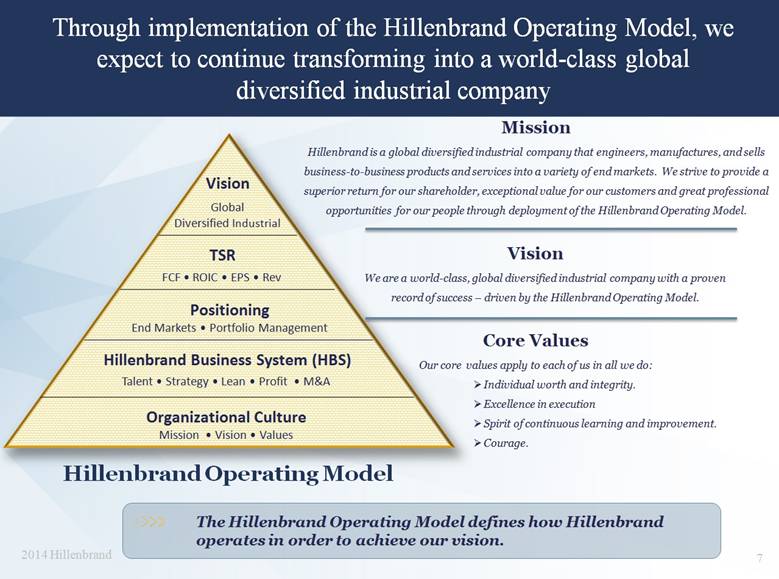

Through implementation of the Hillenbrand Operating Model, we expect to continue transforming into a world-class global diversified industrial company 7 Organizational Culture Mission • Vision • Values Mission Hillenbrand is a global diversified industrial company that engineers, manufactures, and sells business-to-business products and services into a variety of end markets. We strive to provide a superior return for our shareholder, exceptional value for our customers and great professional opportunities for our people through deployment of the Hillenbrand Operating Model. The Hillenbrand Operating Model defines how Hillenbrand operates in order to achieve our vision. Vision We are a world-class, global diversified industrial company with a proven record of success – driven by the Hillenbrand Operating Model. Core Values Our core values apply to each of us in all we do: Individual worth and integrity. Excellence in execution Spirit of continuous learning and improvement. Courage. Hillenbrand Operating Model |

|

|

Two attractive platforms provide robust revenue growth Multiple pathways/end markets for growth Diversified revenue sources Parts and service revenue ~ 1/3 of total Historical Adj EBITDA* margin > 25% Strong, predictable cash flow Batesville *See Appendix for reconciliation TerraSource Process Equipment Group 8 (K-Tron merged with Coperion effective 10/1/2013) $0 $300 $600 $900 $1,200 $1,500 $1,800 FY10 FY11 FY12 FY13 FY14E Revenue Since 2010 $ millions |

|

|

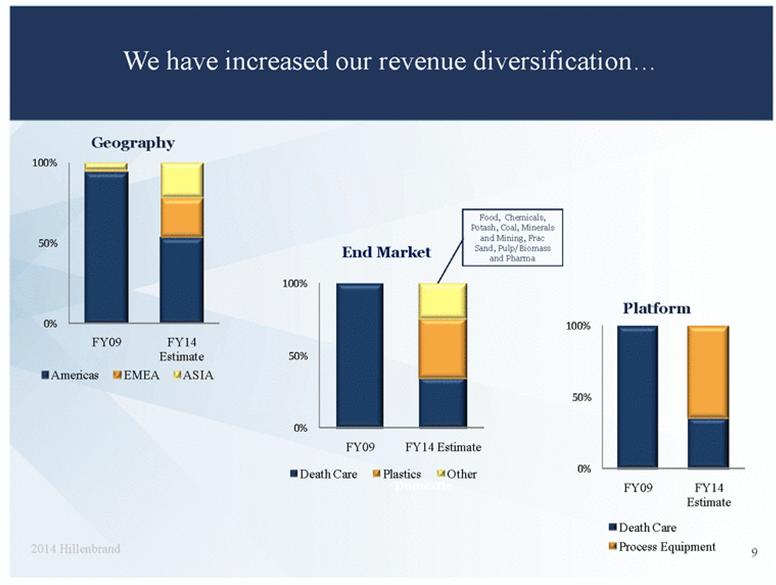

We have increased our revenue diversification Geography Platform Domestic End Market Food, Chemicals, Potash, Coal, Minerals and Mining, Frac Sand, Pulp/Biomass and Pharma 9 0% 50% 100% FY09 FY14 Estimate Death Care Process Equipment 0% 50% 100% FY09 FY14 Estimate Death Care Plastics Other |

|

|

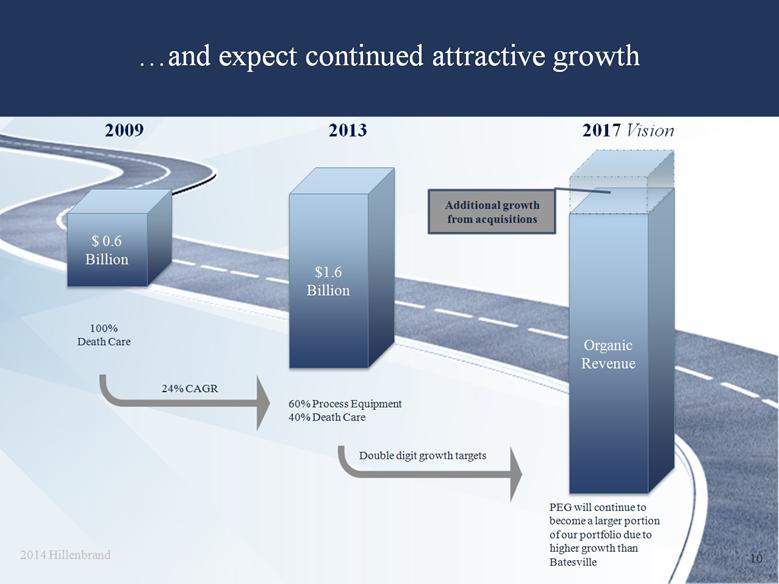

and expect continued attractive growth $ 0.6 Billion 2013 2017 Vision 2009 $1.6 Billion Organic Revenue 24% CAGR 60% Process Equipment 40% Death Care Double digit growth targets 100% Death Care PEG will continue to become a larger portion of our portfolio due to higher growth than Batesville Additional growth from acquisitions 10 |

|

|

Process Equipment Group Overview 11 |

|

|

Our Process Equipment Group companies manufacture mission critical world-class industrial equipment Rotex Separating equipment Sizing equipment Service and parts Crushers Materials handling equipment Service and parts TerraSource Global Compounders and extruders Materials handling equipment Feeders and components System solutions Service and parts Coperion (K-Tron merged with Coperion effective 10/1/2013) 12 |

|

|

Sampling of Blue Chip Customer Mix and have attractive fundamentals Revenue Mix by Geography* Revenue Mix by Type* Balanced geographic diversification Stable revenue and attractive margins from parts and service business Highly diversified customer base with a strong history of long-term relationships with blue-chip customers Proven products with substantial brand value and recognition, combined with industry-leading applications and engineering expertise PEG Brands * FY 2014 ESTIMATE 13 Parts & Service Machines |

|

|

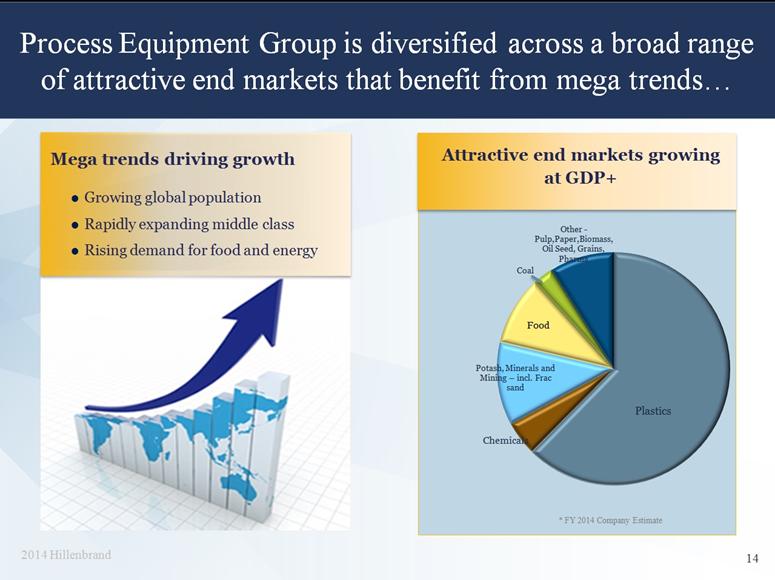

Process Equipment Group is diversified across a broad range of attractive end markets that benefit from mega trends Mega trends driving growth Growing global population Rapidly expanding middle class Rising demand for food and energy Attractive end markets growing at GDP+ * FY 2014 Company Estimate 14 |

|

|

and the strategy focuses on capitalizing on these mega trends to drive growth K-Tron Rotex Terra Source Coperion Develop new products, applications expertise and systems to penetrate growing markets Processed Food Engineered Plastics Establish scope and scale to accelerate global growth Improve access to underpenetrated geographies China India Leverage Coperion’s 29 global locations Leverage Coperion business to accelerate revenue growth K-Tron equipment in Coperion Systems Leverage end market expertise to access new customers and markets Coperion expansion in attractive US market through K-Tron rep. network Enhanced system capabilities Margin expansion through Lean and HBS Brazil Russia Energy Minerals 15 Forest Products Fertilizer |

|

|

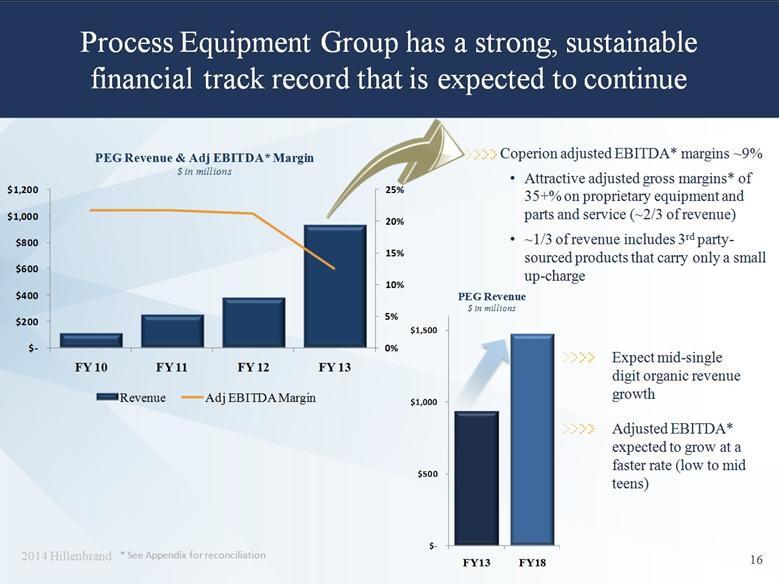

Process Equipment Group has a strong, sustainable financial track record that is expected to continue Expect mid-single digit organic revenue growth Adjusted EBITDA* expected to grow at a faster rate (low to mid teens) * See Appendix for reconciliation Coperion adjusted EBITDA* margins ~9% Attractive adjusted gross margins* of 35+% on proprietary equipment and parts and service (~2/3 of revenue) ~1/3 of revenue includes 3rd party-sourced products that carry only a small up-charge 16 $ - $500 $1,000 $1,500 FY13 FY18 PEG Revenue $ in millions 0% 5% 10% 15% 20% 25% $ - $200 $400 $600 $800 $1,000 $1,200 FY 10 FY 11 FY 12 FY 13 PEG Revenue & Adj EBITDA* Margin $ in millions Revenue Adj EBITDA Margin |

|

|

Batesville Overview 17 |

|

|

Other (100+) Batesville Importers Aurora Matthews Caskets Market Leader Grave Markers Cremation Market Leader Vaults Batesville is the industry leader in the largest and most profitable segment of the North American death care industry North American Death Care ($2.6 Billion Industry) North American Caskets (Total Revenue $1.3 Billion) Batesville (Total 2013 Revenue: $621 Million) Other, including Cremation Options®, Technology Solutions and Northstar Source: Company estimates, industry reports and public filings for FY 2013 Iconic brand with 100+ years of history Superior mix of products Industry leader in volume, revenue and margin share 18 Batesville Caskets |

|

|

Batesville’s strategy is to optimize the casket business, capitalize on growth opportunities and sustain margins Optimize the Profitable Casket Business Maintain Attractive Margins Capitalize on Growth Opportunities New product development Merchandising and consultative selling Cremation Options® products – caskets, containers and urns Technology Solutions – websites & business management software Operational excellence Lean manufacturing and distribution Continuous improvement in all business processes 19 |

|

|

Batesville has predictable strong cash flow and attractive margins Industry Dynamics Attractive Financials Deaths expected to increase in the future as baby boomers age North American cremation rate is currently ~ 46% and increasing approximately 120-140 basis points per year Increase in future deaths expected to be offset by cremation, resulting in relatively flat burial market Historically high return on invested capital Adjusted EBITDA margins* improved in FY13 Relentless focus on lean to maintain attractive margins Revenue & Adj EBITDA Margin Estimated Deaths (Millions) * See Appendix for reconciliation 20 * 0% 5% 10% 15% 20% 25% 30% 35% $ - $200 $400 $600 $800 $1,000 FY 10 FY 11 FY 12 FY 13 Revenue Adj EBITDA margin |

|

|

Financial Results 21 |

|

|

Third quarter consolidated revenue up 2%, adjusted EBITDA* grew 11% driven by improved Process Equipment Group margins. Hillenbrand Q3 2014 Results –Three Months Ended June 30 ($ in millions, except EPS) Q3 FY14 Q3 FY13 Net Revenue % Year-Over-Year Growth $417 2.0% $409 71.5% EBITDA (Adjusted)* % of Revenue $71 17.0% $64 15.6% EPS (Adjusted)* $0.57 $0.48 Free Cash Flow** $48 $23 * See Appendix for reconciliation **Free cash flow is defined as operating cash flow less capital expenditures – See Appendix for reconciliation 22 Process Equipment Group revenue grew 5% with growth demonstrated throughout the business. Backlog increased 2% sequentially to $731 million Batesville revenue declined 4% driven by decreased volume due to a lower number of North American burials and lower average selling prices. Adjusted EBITDA* grew 11% primarily due to: $11million increase in Process Equipment Group EBITDA resulting from improved margins $2 million decrease in Batesville EBITDA due to lower volume and lower average selling prices. |

|

|

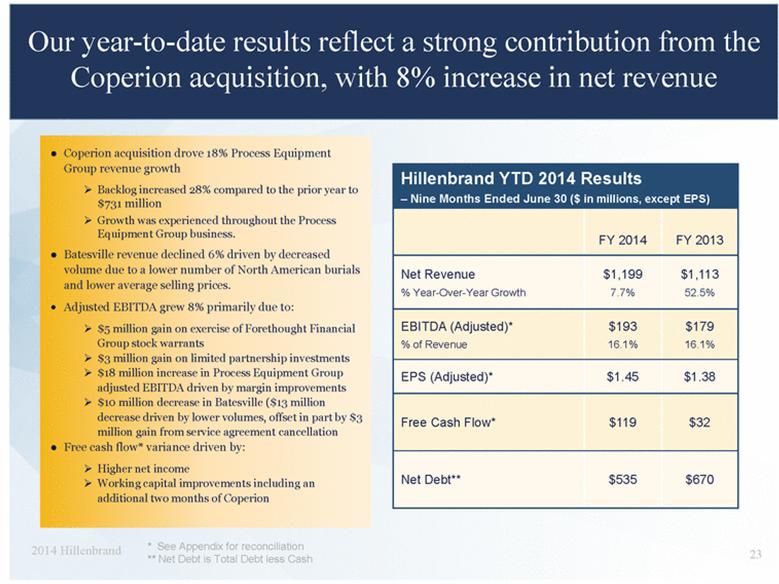

Our year-to-date results reflect a strong contribution from the Coperion acquisition, with 8% increase in net revenue Hillenbrand YTD 2014 Results – Nine Months Ended June 30 ($ in millions, except EPS) FY 2014 FY 2013 Net Revenue % Year-Over-Year Growth $1,199 7.7% $1,113 52.5% EBITDA (Adjusted)* % of Revenue $193 16.1% $179 16.1% EPS (Adjusted)* $1.45 $1.38 Free Cash Flow* $119 $32 Net Debt** $535 $670 * See Appendix for reconciliation ** Net Debt is Total Debt less Cash 23 Coperion acquisition drove 18% Process Equipment Group revenue growth Backlog increased 28% compared to the prior year to $731 million Growth was experienced throughout the Process Equipment Group business. Batesville revenue declined 6% driven by decreased volume due to a lower number of North American burials and lower average selling prices. Adjusted EBITDA grew 8% primarily due to: $5 million gain on exercise of Forethought Financial Group stock warrants $3 million gain on limited partnership investments $18 million increase in Process Equipment Group adjusted EBITDA driven by margin improvements $10 million decrease in Batesville ($13 million decrease driven by lower volumes, offset in part by $3 million gain from service agreement cancellation Free cash flow* variance driven by: Higher net income Working capital improvements including an additional two months of Coperion |

|

|

Hillenbrand has a history of strong financial performance ** *** Net Debt is Total Debt less Cash 24 ** ** See Appendix for reconciliation FY10 includes K-Tron acquisition ($369m Net purchase price) FY11 includes Rotex acquisition ($240m Net purchase price) FY13 includes Coperion acquisition ($512m Net purchase price, including $130m pension liability) *See Appendix for reconciliation * $0 $100 $200 FY10 FY11 FY12 FY13 Free Cash Flow Base FCF Forethought $ - $500 $1,000 $1,500 $2,000 FY 10 FY 11 FY 12 FY 13 Revenue $ in millions $0 $100 $200 $300 $400 $500 $600 $700 $800 FY10 FY11 FY12 FY13 Net Debt $ - $100 $200 $300 FY 10 FY 11 FY 12 FY 13 Adjusted EBITDA $ in millions |

|

|

which fuels a capital deployment strategy that focuses on creating shareholder value Reinvestment for long-term growth Organic growth investments Acquisitions Meaningful dividend $0.79 per share in 2014 (39% payout ratio using mid-point EPS guidance) Annual $0.01 increase per share per year (6 consecutive years) Attractive dividend yield: 2.4% (9/3/14) Reinvestment for Long-Term Growth Working Capital and CapEx Dividends 25 |

|

|

and we expect attractive revenue and earnings growth in 2014 2014 Guidance Summary 2013 2014 Revenue (millions) $1,553 $1,700 Adjusted EPS* $1.88 $2.00 - $2.10 * See Appendix for reconciliation 26 |

|

|

Hillenbrand is an attractive investment opportunity Market leading platforms with robust cash generation Strong balance sheet and cash flow Process Equipment Group represents ~2/3 of Hillenbrand revenue with attractive organic mid to high single-digit growth expected Bottom-line growth enhanced by leveraging core competencies Meaningful return of cash to shareholders, including an attractive dividend yield Annual dividend increases since HI inception (2008) Strong Financial Profile Growth Opportunity Compelling Dividend Proven Track Record Demonstrated acquisition success Proven, results-oriented management teams Strong core competencies in lean business, strategy management and talent development 27 |

|

|

Thank you for joining us today 28 Questions? |

|

|

Appendix 29 |

|

|

Disclosure regarding non-GAAP measures While we report financial results in accordance with accounting principles generally accepted in the United States (GAAP), we also provide certain non-GAAP operating performance measures. These non-GAAP measures are referred to as “adjusted” and exclude expenses associated with backlog amortization, inventory step-up, business acquisition and integration, restructuring, and antitrust litigation. The related incom tax for all of these items is also excluded. This non-GAAP information is provided as a supplement, not as a substitute for, or as superior to, measures of financial performance prepared in accordance with GAAP. One important non-GAAP measure that we use is Adjusted Earnings Before Interest, Income Tax, Depreciation, and Amortization (“Adjusted EBITDA”). As previously discussed, a part of our strategy is to selectively acquire companies that we believe can benefit from our core competencies to spur faster and more profitable growth. Given that strategy, it is a natural consequence to incur related expenses, such as amortization from acquired intangible assets and additional interest expense from debt-funded acquisitions. Accordingly, we use Adjusted EBITDA, among other measures, to monitor our business performance. Another important non-GAAP measure that we use is backlog. Backlog is not a term recognized under GAAP; however, it is a common measurement used in the Process Equipment Group industry. Our backlog represents the amount of consolidated revenue that we expect to realize on contracts awarded related to the Process Equipment Group. Backlog includes expected revenue from large systems, equipment, and to a lesser extent, replacement parts, components, and service. We use this non-GAAP information internally to make operating decisions and believe it is helpful to investors because it allows more meaningful period-to-period comparisons of our ongoing operating results. The information can also be used to perform trend analysis and to better identify operating trends that may otherwise be masked or distorted by these types of items. Finally, the Company believes such information provides a higher degree of transparency. 30 |

|

|

Q3 FY14 & Q3 FY13 - Adjusted EBITDA to consolidated net income reconciliation ($ in millions) 31 2014 2013 Adjusted EBITDA: Process Equipment Group 44.1 $ 33.3 $ Batesville 34.3 36.7 Corporate (7.6) (6.3) Less: Interest income (0.3) - Interest expense 5.6 5.9 Income tax expense 12.7 5.8 Depreciation and amortization 14.7 27.4 Business acquisition and integration 1.7 2.4 Inventory step-up - 8.0 Restructuring 1.6 0.3 Litigation 1.4 0.2 Consolidated net income 33.4 $ 13.7 $ Three months ended June 30, |

|

|

YTD FY14 & FY13 - Adjusted EBITDA to consolidated net income reconciliation ($ in millions) 32 2014 2013 Adjusted EBITDA: Process Equipment Group 96.8 $ 78.5 $ Batesville 113.7 123.6 Corporate (17.3) (22.8) Less: Interest income (0.6) (0.3) Interest expense 17.5 17.2 Income tax expense 35.4 17.0 Depreciation and amortization 43.7 70.3 Business acquisition and integration 4.7 12.4 Inventory step-up - 18.7 Restructuring 2.8 2.2 Litigation 1.4 0.3 Consolidated net income 88.3 $ 41.5 $ Nine months ended June 30, |

|

|

Q2 FY14 & Q2 FY13 - Adjusted EBITDA to consolidated net income reconciliation ($ in millions) 33 2014 2013 Adjusted EBITDA: Process Equipment Group 26.0 $ 24.2 $ Batesville 44.9 48.4 Corporate (1.7) (8.5) Less: Interest income (0.1) (0.2) Interest expense 5.6 6.8 Income tax expense 13.7 5.3 Depreciation and amortization 14.7 27.8 Business acquisition and integration 1.1 1.8 Inventory step-up - 8.1 Restructuring 0.9 1.3 Antitrust litigation - - Consolidated net income 33.3 $ 13.2 $ Three months ended March 31, |

|

|

Q1 FY14 & Q1 FY13 - Adjusted EBITDA to consolidated net income reconciliation ($ in millions) 34 2013 2012 Adjusted EBITDA: Process Equipment Group 26.7 $ 20.9 $ Batesville 34.5 38.5 Corporate (8.0) (8.0) Less: Interest income (0.2) (0.1) Interest expense 6.3 4.5 Income tax expense 9.0 5.9 Depreciation and amortization 14.3 15.0 Business acquisition and integration 1.9 8.2 Inventory step-up - 2.6 Restructuring 0.3 0.6 Antitrust litigation - 0.1 Consolidated net income 21.6 $ 14.6 $ Three months ended December 31, |

|

|

Adjusted EBITDA to consolidated net income reconciliation ($ in millions) 35 2013 2012 2011 2010 Adjusted EBITDA: Process Equipment Group 116.4 $ 79.7 $ 53.3 $ 23.6 $ Batesville 161.0 152.8 179.9 195.0 Corporate (29.9) (25.1) (24.8) (27.4) Less: Interest income (0.6) (0.5) $ (7.4) $ (13.0) $ Interest expense 24.0 12.4 11.0 4.2 Income tax expense 28.3 30.1 51.7 54.1 Depreciation and amortization 89.4 40.4 36.1 28.2 Business acquisition and integration 16.0 4.2 6.3 10.5 Inventory step-up 21.8 - 2.8 11.6 Restructuring 2.8 8.3 1.3 3.0 Antitrust 0.2 5.5 1.3 5.0 Other 0.2 - (0.8) (4.7) Long-term incentive compensation related to the international integration - 2.2 - - Consolidated net income 65.4 $ 104.8 $ 106.1 $ 92.3 $ Years Ended September 30, |

|

|

Q3 FY14 & Q3 FY13 Non-GAAP Operating Performance Measures ($ in millions) 36 GAAP Adj Adjusted GAAP Adj Adjusted Cost of goods sold 267.5 $ 0.1 $ (a) 267.6 $ 276.0 $ (8.6) $ (c) 267.4 $ Operating expenses 97.7 (4.7) (b) 93.0 107.1 (15.6) (d) 91.5 Interest expense 5.6 - 5.6 5.9 (0.5) (e) 5.4 Other income (expense), net 0.1 - 0.1 (0.3) (0.2) (f) (0.5) Income tax expense 12.7 1.3 (m) 14.0 5.8 7.4 (m) 13.2 Net income 1 32.8 3.3 36.1 13.3 17.1 30.4 Diluted EPS 0.51 0.06 0.57 0.21 0.27 0.48 1 Net income attributable to Hillenbrand P = Process Equipment Group; B = Batesville; C = Corporate (a) Restructuring costs ($0.1 reduction B) (b) Business acquisition and integration costs ($0.5 P, $1.2 C), litigation costs ($1.4 B), restructuring costs ($1.5 P, $0.1 C) (c) Inventory step up ($8.0 P), restructuring costs ($0.1 P, $0.5 B) (d) Business acquisition and integration costs ($1.0 P, $1.5 C), backlog amortization ($12.8 P), restructuring costs ($0.2 P), other ($0.1 B) (e) Business acquisition and integration costs ($0.5 C) (f) Business acquisition and integration costs ($0.2 C) (m) Tax effect of adjustments 2013 2014 Three months ended June 30, |

|

|

YTD FY14 & FY13 Non-GAAP Operating Performance Measures ($ in millions) 37 GAAP Adj Adjusted GAAP Adj Adjusted Cost of goods sold 775.4 $ 0.2 $ (a) 775.6 $ 735.2 $ (21.3) $ (c) 713.9 $ Operating expenses 291.6 (9.1) (b) 282.5 301.9 (44.4) (d) 257.5 Interest expense 17.5 - 17.5 17.2 (1.1) (e) 16.1 Other income (expense), net 9.7 - 9.7 0.3 (1.1) (f) (0.8) Income tax expense 35.4 2.6 (g) 38.0 17.0 19.2 (g) 36.2 Net income 1 86.1 6.3 92.4 40.3 46.5 86.8 Diluted EPS 1.35 0.10 1.45 0.64 0.74 1.38 1 Net income attributable to Hillenbrand P = Process Equipment Group; B = Batesville; C = Corporate (a) Restructuring costs ($0.1 P, $0.3 reduction B) (b) Business acquisition and integration costs ($1.5 P, $3.2 C), litigation costs ($1.4 B), restructuring costs ($1.7 P, $1.3 C) (c) Inventory step up ($18.7 P), restructuring costs ($0.3 P, $2.3 B) (d) Business acquisition and integration costs ($1.3 P, $12.1 C), backlog amortization ($29.9 P), restructuring ($0.2 P, $0.5 B, $0.2 C), litigation costs ($0.1 B), other ($0.1 B) (e) Business acquisition and integration costs ($1.1 C) (f) Acquisition-related foreign currency transactions ($0.8 C), business acquisition and integration costs ($0.2 C), other ($0.1 B) (g) Tax effect of adjustments 2014 2013 Nine months ended June 30, |

|

|

Q2 FY14 & Q2 FY13 Non-GAAP Operating Performance Measures ($ in millions) 38 GAAP Adj Adjusted GAAP Adj Adjusted Cost of goods sold 254.0 $ 0.2 $ (a) 254.2 $ 264.5 $ (9.7) $ (d) 254.8 $ Operating expenses 99.9 (2.3) (b) 97.6 108.4 (15.2) (e) 93.2 Interest expense 5.6 - 5.6 6.8 (0.6) (f) 6.2 Other income (expense), net 9.7 - 9.7 (0.3) - (0.3) Income tax expense 13.7 0.7 (c) 14.4 5.3 7.6 (c) 12.9 Net income 1 33.0 1.4 34.4 12.7 17.9 30.6 Diluted EPS 0.51 0.03 0.54 0.20 0.29 0.49 1 Net income attributable to Hillenbrand P = Process Equipment Group; B = Batesville; C = Corporate (a) Restructuring ($0.1 P, $0.3 credit B) (b) Business acquisition and integration costs ($0.3P, $0.8 C), restructuring ($1.2 C) (c) Tax effect of adjustments (d) Inventory step up ($8.1 P), restructuring ($0.1 P, $1.5 B) (e) Business acquisition and integration costs ($0.3 P, $1.6 C), backlog amortization ($12.9 P), restructuring ($0.4 B) (f) Business acquisition and integration costs ($0.6 C) 2014 Three months ended March 31, 2013 |

|

|

Q1 FY14 & Q1 FY13 Non-GAAP Operating Performance Measures ($ in millions) 39 GAAP Adj Adjusted GAAP Adj Adjusted Cost of goods sold 253.9 $ (0.1) $ (a) 253.8 $ 194.7 $ (3.0) $ (d) 191.7 $ Operating expenses 94.0 (2.1) (b) 91.9 86.4 (13.6) (e) 72.8 Interest expense 6.3 - 6.3 4.5 - 4.5 Other income (expense), net (0.1) - (0.1) 0.9 (0.9) (f) - Income tax expense 9.0 0.6 (c) 9.6 5.9 4.2 (c) 10.1 Net income 1 20.3 1.6 21.9 14.3 11.5 25.8 Diluted EPS 0.32 0.02 0.34 0.23 0.18 0.41 1 Net income attributable to Hillenbrand P = Process Equipment Group; B = Batesville; C = Corporate (a) Restructuring ($0.1 B) (b) Business acquisition and integration costs ($0.7 P, $1.2 C), restructuring ($0.2 P) (c) Tax effect of adjustments (d) Inventory step up ($2.6 P), restructuring ($0.1 P, $0.3 B) (e) Business acquisition costs ($9.0 C), backlog amortization ($4.2 P), restructuring ($0.2 C), antitrust litigation ($0.1 B), other ($0.1 B) (f) Acquisition-related foreign currency transactions ($0.8 C), other ($0.1 B) Three months ended December 31, 2013 2012 |

|

|

Non-GAAP Operating Performance Measures ($ in millions) 40 Adj Adj GAAP Adj Adj $ 1,034.7 $ (25.2) (a) $ 1,009.5 $ 594.3 $ (4.2) (f) $ 590.1 $ 513.5 $ (2.8) (i) $ 510.7 $ 435.9 $ (11.6) (l) $ 424.3 400.6 (52.5) (b) 348.1 240.1 (18.8) (g) 221.3 211.3 (8.9) (j) 202.4 175.4 (15.5) (m) 159.9 24.0 (1.2) (c) 22.8 12.4 - 12.4 11.0 - 11.0 4.2 - 4.2 (0.4) (1.1) (d) (1.5) (1.5) - (1.5) 10.2 - 10.2 12.7 - 12.7 28.3 22.9 (e) 51.2 30.1 18.1 (h) 48.2 51.7 4.0 (k) 55.7 54.1 7.8 (n) 61.9 54.9 4.9 106.1 7.7 113.8 92.3 19.3 111.6 1.01 0.87 1.88 1.68 0.08 1.76 1.71 0.13 1.84 1.49 0.31 1.80 1 Net income attributable to Hillenbrand (a) Inventory step-up ($21.8 P), restructuring ($0.3 P, $2.9 B), business acquisition costs ($0.2 P) (b) Backlog amortization ($34.5 P), business acquisition costs ($3.1 P, $13.7 C), restructuring ($0.2 P, $0.5 B, $0.2 C), antitrust litigation ($0.2 B), other ($0.1 B) (c) Business acquisition costs ($1.2 C) (d) Acquisition related foreign currency transactions ($0.8C), business acquisition costs ($0.2 C), other ($0.1B) (e) Tax effect of adjustments (f) Restructuring ($0.9 P, $3.3 B) (g) (h) Tax benefit of the international integration ($10.4), tax effect of adjustments ($7.7) (i) Inventory step-up ($2.8 P) (j) Restructuring ($1.3 B), antitrust litigation ($1.3 B), business acquisition costs ($0.3 P, $6.0 C), backlog amortization ($0.8 P), sales tax recoveries ($0.8 B) (k) Tax effect of adjustments (l) Inventory step-up ($11.6 P) (m) (n) Tax effect of adjustments 2012 2010 2011 Adjusted Adjusted Cost of goods sold Operating expenses GAAP Adjusted GAAP Interest expense 109.7 P = Process Equipment Group; B = Batesville; C = Corporate Diluted EPS Income tax expense Net income 1 104.8 Other income (expense), net Business acquisition costs ($0.3 P, $10.2 C), antitrust litigation ($5.0 B), restructuring ($3.0 C),Backlog amortization ($1.7 P), LESS sales tax recoveries ($4.7). Antitrust litigation ($5.5 B), restructuring ($2.8 P, $0.6 B, $0.9 C), business acquisition costs ($4.2 C), backlog amortization ($2.5 P), long–term incentive compensation related to the international integration ($0.2 P, $0.8 B, $1.2 C), other ($0.1 B) Years Ended September 30, 118.3 2013 GAAP Adjusted 63.4 |

|

|

Q3 FY14 & Q3 FY13 - Cash Flow Information ($ in millions) 41 Operating Activities 2014 2013 Consolidated net income 33.4 $ 13.7 $ Depreciation and amortization 14.7 27.4 Change in working capital (3.2) (1.7) Other, net 9.8 (8.3) Net cash provided by operating activities (A) 54.7 $ 31.1 $ Capital expenditures (B) (6.5) (7.9) Acquisition of business, net of cash acquired - (0.1) Debt activity (28.9) (11.4) Dividends (12.4) (12.2) Other 0.8 0.9 Net change in cash 7.7 $ 0.4 $ Free Cash Flow (A-B) 48.2 $ 23.2 $ Three months ended June 30, |

|

|

YTD FY14 and FY13 - Cash Flow Information ($ in millions) 42 Operating Activities 2014 2013 Consolidated net income 88.3 $ 41.5 $ Depreciation and amortization 43.7 70.3 Change in working capital 20.4 0.1 Other, net (15.5) (61.1) Net cash provided by operating activities (A) 136.9 $ 50.8 $ Capital expenditures (B) (17.9) (19.1) Acquisition of business, net of cash acquired - (415.7) Debt activity (68.9) 437.3 Dividends (37.2) (36.5) Other 6.1 4.1 Net change in cash 19.0 $ 20.9 $ Free Cash Flow (A-B) 119.0 $ 31.7 $ Nine months ended June 30, |

|

|

Q2 FY14 & Q2 FY13 - Cash Flow Information ($ in millions) 43 Operating Activities 2014 2013 Consolidated net income 33.3 $ 13.2 $ Depreciation and amortization 14.7 27.9 Change in working capital 1.5 (11.1) Other, net (13.2) (30.0) Net cash provided by operating activities (A) 36.3 $ - $ Capital expenditures (B) (5.8) (5.6) Acquisition of business, net of cash acquired - - Debt activity (25.8) (46.1) Dividends (12.4) (12.2) Other (3.6) 2.5 Net change in cash (11.3) $ (61.4) $ Free Cash Flow (A-B) 30.5 $ (5.6) $ Three months ended March 31, |

|

|

Q1 FY14 & Q1 FY13 - Cash Flow Information ($ in millions) 44 Operating Activities 2013 2012 Consolidated net income 21.6 $ 14.6 $ Depreciation and amortization 14.3 15.0 Change in working capital 22.1 12.9 Other, net (12.1) (22.8) Net cash provided by operating activities (A) 45.9 $ 19.7 $ Capital expenditures (B) (5.6) (5.6) Acquisition of businesses, net of cash acquired - (415.6) Debt activity (14.2) 494.8 Dividends (12.4) (12.1) Other 5.9 0.7 Net change in cash 19.6 $ 81.9 $ Free Cash Flow (A-B) 40.3 $ 14.1 $ Three months ended December 31, |

|

|

Cash Flow Information ($ in millions) 45 Operating Activities 2013 2012 2011 2010 Consolidated net income 65.4 $ 104.8 $ 106.1 $ 92.3 $ Depreciation and amortization 89.4 40.4 36.1 28.2 Interest income on Forethought Note - - (6.4) (12.0) Forethought Note interest payment - - 59.7 10.0 Change in working capital (12.3) (19.8) (16.4) 16.9 Other, net (15.3) 12.8 10.4 (17.2) Net cash provided by operating activities (A) 127.2 $ 138.2 $ 189.5 $ 118.2 $ Capital expenditures (B) (29.9) (20.9) (21.9) (16.3) Forethought Note principal repayment - - 91.5 - Acquisition of businesses, net of cash acquired (415.7) (4.4) (240.9) (371.5) Proceeds from redemption and sales, and ARS and investments 1.7 0.8 12.4 37.2 Debt activity 385.6 (162.3) 28.1 334.2 Dividends (48.7) (47.6) (46.9) (46.2) Purchase of common stock - - (3.8) - Other 2.3 0.9 9.1 7.6 Net change in cash 22.5 $ (95.3) $ 17.1 $ 63.2 $ Free Cash Flow (A-B) 97.3 $ 117.3 $ 167.6 $ 101.9 $ Years Ended September 30, |